EDSX – European Digital Assets Exchange

EDSX – European Digital Assets Exchange

Corporate finance describes financial decisions of corporations; its main objective is to maximize corporate value while reducing financial risk. The financial manager takes responsibility for the corporate finance decisions.

Cash flows refer to the excess of cash revenues over cash outlays, they are usually measured during a specified period of time.

A balance sheet can be analyzed either from a capital-employed perspective or from a solvency-and-liquidity perspective.

The working capital is the net balance of operating uses and sources of funds; if uses of funds exceed sources of funds, the balance is positive and working capital needs to be financed, if negative, it represents a source of funds generated by the operating cycle.

Two main formats of income statement are frequently used, which differ in the way they present revenues and expenses related to the operating and investment cycles. They may be presented either by function or by nature.

The aim of financial analysis is to explain how a company can create value in the medium term (shareholders’ viewpoint) or to determine whether it is solvent (lenders’ standpoint).

Either way, the techniques applied in financial analysis are the same.

Operating profit or EBIT represents the earnings generated by investment and operating cycles for a given period.

Operating leverage links variation in activity (measured by sales) with variations in result (either operating profit or net income). Operating leverage depends on the level and nature of the breakeven point.

Analyzing the credit risk of a company, means to analyze how the company is financed. This can be performed either by looking at several fiscal years, or on the basis of the latest available balance sheet.

We can measure profitability only by studying returns in relation to the invested capital. If no capital is invested, there is no profitability to speak of.

The leverage effect is the difference between return on equity and return on capital employed. Although it can lift a company’s return on equity above return on capital employed, it can also depress it, turning the dream into a nightmare.

An efficient market is one in which the prices of financial securities at any time rapidly reflect all available relevant information. The terms “perfect market” or “market in equilibrium” are synonymous with “efficient market”.

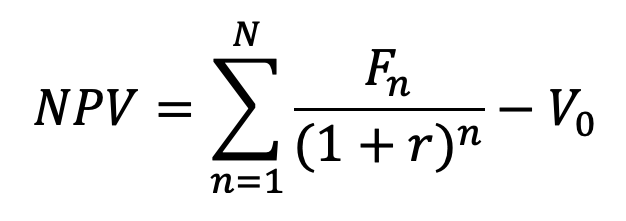

To discount means to calculate the present value of a future cash flow.

The tools used for measuring creation of value can be classified under three headings:

Net present value (NPV) is the difference between present value and market value (V0):

The discounting rate that makes net present value equal to zero is called the “internal rate of return (IRR)” or “yield to maturity”.

Risk is the probability that the outcome results in a loss. In a pure risk situation a gain never occurs; in a speculative risk situation a gain or a loss may occur.

There is a tradeoff between risk and return, low risks are associated with low potential returns, whereas high risks are associated with high potential returns.

Expected outcome E(r), is a measure of expected return, and standard deviation![]() (r) measures the average dispersion of returns around expected outcome, in other words, risk.

(r) measures the average dispersion of returns around expected outcome, in other words, risk.

Diversification means that investors do not concentrate their entire wealth in only one financial asset, because they prefer to hold well-diversified portfolios. This has the effect to reduce the risk of the investor’s portfolio.

The efficient frontier shows all the portfolios that offer investors the best risk-return ratio (i.e. minimal risk for a given return).

The capital market line links the market portfolio M to the risk-free asset. For a given level of risk, no portfolio is better than those located on this line.

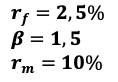

The CAPM is a financial model and it says that if all investors hold the market portfolio, the risk premium they will demand is proportional to market beta.

The beta measures a security’s sensitivity to market risk.

Example

Then, the required rate of return is:

![]()

The cost of capital is the minimum rate of return on the company’s investments that can satisfy both shareholders (the cost of equity) and debt holders (the cost of debt). The cost of capital is thus the company’s total cost of financing.

Share analysis is centered on changes in stock market prices, multiples (especially P/E), dividends and returns, compared with required returns.

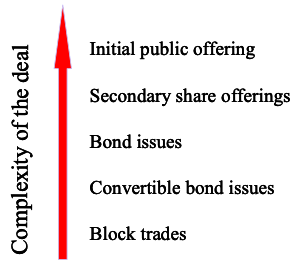

The company’s main goal in selling its securities to investors is to obtain the highest possible price.

For the sale to be successful, the company must offer investors a return or a potential capital gain. Otherwise, it will be harder to gain access to the market in the future.

Example: The type of offering:

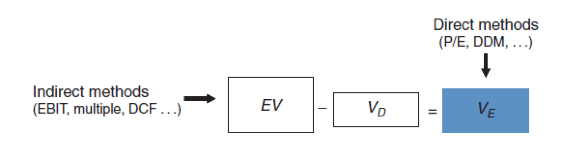

There are two methods used to value equity: the direct method and the indirect method. In the direct method, obviously, we value equity directly. In the indirect method, we first value the firm as a whole (what we call “enterprise” or “firm” Value), then subtract the value of net debt to get the equity value.

Example

The Discounted Cash Flow (DCF) method consists of applying the investment decision techniques to the firm value calculation, discounting a series of future cash flows.

The peer comparison or multiples approach is based on three fundamental principles:

– the company is to be valued in its entirety;

– the company is valued at a multiple of its profit-generating capacity. The most commonly used are the P/E ratio, EBITDA and EBIT multiples;

– markets are efficient and comparisons are therefore justified.

Example: Consider the following two similarly-sized companies, Ann and Valeria, operating in the same sector and enjoying the same outlook for the future, with the following characteristics:

|

Company |

Ann |

Valeria |

|

Operating income |

150 |

177 |

|

– Interest expense |

30 |

120 |

|

– Corporate income tax (40%) |

48 |

23 |

|

= Net Profit |

72 |

34 |

|

Market capitalization |

1800 |

? |

|

Value of debt (at 10% p. a.) |

300 |

1200 |

As Ann’s NOPAT is 150×( 1−40%)= 90, the multiple of Ann’s NOPAT is 2100/90 = 23.3. Valeria’s enterprise value is therefore equal to 23.3 times its NOPAT, or 23.3 × 106 = 2470. We now subtract the value of the debt (1200) to obtain the value of equity capital, or 1270.

Companies design their debt funding considering:

FUNDAMENTAL FACTORS

COSTS OF DEBT

EXTENDED TRADEOFF MODEL

Generally excess cash can be used for:

A company may in certain circumstances buy back its own shares and either keep them on the balance sheet or cancel them, in which case there is said to be a capital decrease or capital reduction.

Dilution of control is the reduction of rights in the company sustained by a shareholder for which the capital increase entails neither an outflow nor an inflow of funds.

There are seven different type of shareholders:

A stock exchange listing offers distinct benefits: it enables financial managers to access capital markets and obtain the market value for their companies.

The control premium is the amount a buyer is ready to pay over the current market value in order to obtain the control of a company.

The minority discount is a reduction from the market value accepted by minority shareholders in order to sell their stocks.

Corporate governance is the organization of the control over and management of a firm. A narrower definition of corporate governance covers the relationship between the firm’s shareholders and management, mainly involving the functioning of the board of directors or the supervisory board.

For a private company the key is the art of negotiation that consists of allocating the value of the synergies expected from a merger or acquisition between the buyer and the seller.

For a public company the procedure is generally more complex. Stake-building can be the first step to acquiring control over a listed company. But it can be slow and faces the requirement of declaring the crossing of thresholds. A public offer is the usual way to acquire a listed company. It can be in cash or in shares, hostile or friendly, voluntary or mandatory.

Value is created only when the sum of cash flows from the two investments is higher because they are both managed by the same group. This is the result of industrial synergies (2 + 2 = 5), and not financial synergies, which do not exist.

A demerger is a separation of the activities of a group: the original shareholders become the shareholders of the separated companies.

In a splitoff, shareholders have the option to exchange their shares in the parent company for shares in a subsidiary.

A Leveraged Buyout (LBO) is the acquisition of a company by one or several private equity funds which finance their purchase mainly by debt.

There are five main categories of financial risk: